Automotive Semiconductor Market Challenges – The EV Revolution

The impact on repair networks and supply chain longevity

The automotive industry is facing a supply chain evolution in the coming years.

The increasing semiconductor value in the overall vehicle cost. Allied Market Research estimated the total automotive semiconductor market to be roughly $38 billion in 2020. It is expected to grow to $114 billion by the end of 2030, implying a compound annual growth of 11.8%, much of this due to the switch to Electric Vehicles (EVs). For example, the drivetrain in an internal combustion car uses approximately $100 of semiconductors, while its EV equivalent uses over $1,000/car (McKinsey).

After-market support. The overall value of the automotive aftermarket is set to rise 33% by 2030 from its existing value of $900 billion. The conversion to electric vehicles (EVs) will require new after-market skill sets and structures, leading to a redistribution of aftermarket profits along the value chain. In numerous countries, legislation around the “Right to Repair” will influence sub-system designs.

Balancing semiconductor supply chains across the Petrol and EV changeover. Managing supply longevity and semiconductor obsolescence to cover up to 10 years of production and 15 years after sales is vital to determining future success.

Factors driving automotive semiconductor obsolescence

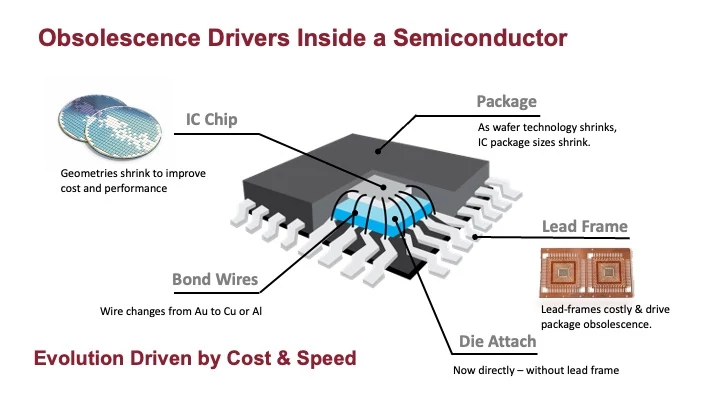

Moore's law predicts that the number of transistors on a microchip or a computer processor will double every two years - with a consequential reduction in the cost per transistor. Its prediction has been accurate since 1975. Constant technological evolution and the exponential rise in the cost of new fab investments means that older and less efficient technologies are starved of investment and eventually discontinued.

As process nodes shrink, maximizing the number of die on a given wafer and improving the device speed, performance, and cost, older geometries and fabs are closed, and Original Component Manufacturers’ (OCMs) resources are re-targeted. The dominant position of third-party fabs in the worldwide semiconductor supply chain means that the decision to discontinue a fab process is often outside the control of the OCM.

Small die sizes and significant fab capital investments mean that production Minimum Order Quantities (MOQs) to justify the process become so large that only the largest consumer OEMs and applications will dictate the longevity of the fab process in the future. Consumer electronics accounts for 80% of the worldwide semiconductor market, while automotive electronics accounts for just 8%.

As die sizes reduce, overall IC package sizes shrink, reducing unit cost. Assembly becomes increasingly automated, and material and investment-heavy piece parts such as lead frames can be replaced with direct die-attach assembly, further improving performance and reducing cost. Older semiconductor package styles such as PDIP, PLCC, TSSOP, and small outline SO packages are less economical and are therefore pruned. Third-party assembly houses also control a significant portion of the semiconductor packaging market, and like 3rd party fabs, they often control component End-of-Life (EOL) dates.

Semiconductor Obsolescence – Changes Post-Allocation

Semiconductor allocation hit automotive manufacturers hard. COVID-19 worries reduced confidence in future demand. Semiconductor production capacity reserved for automotive manufacturers was released and driven by home-working; consumer and communication applications immediately swallowed the spare capacity. When automotive demand returned sooner than expected, semiconductor production capacity was taken, and automotive manufacturers suddenly faced 52-week+ lead times. By their nature, the industry-wide “just-in-time” supply chain models had little built-in security, and automotive production worldwide suffered 12-18 months of production stops and delays.

A period of exceptional demand over and above the capacity to supply always encourages all parts of the supply chain to focus their limited resources on the most profitable products. As the market eventually returns to over-supply, less profitable lines are pruned. Third-party assemblers and fab houses make their own profit/loss calculations and add a discontinuation node outside the direct control of the OCM. Z2Data reports:

- A 30% increase in overall component discontinuations pre- and post-allocation.

- That 30%+ of all discontinuations are not flagged in advance and move from active status with predicted longevity to immediate LTB (Last Time Buy).

- Ultra-short LTB windows are also increasingly common as third parties make unilateral wafer-fab decisions, and sudden assembly tooling failures are not replaced.

This supply re-alignment has coincided with a fundamental technology shift that has driven a vast increase in automotive semiconductor usage to electric vehicles. This includes electrifying the drive automation system, charger, inverter, DC/DC converter, high-voltage battery, central processor, motor, autonomous driving, and infotainment systems. Power electronics is based on substantial new investments in Si, SiC, and GaN technologies, and processor electronics is based on faster, less power-hungry technologies.

There continues to be uncertainty surrounding the ongoing after-market needs of the petrol/diesel platforms and their older semiconductor technologies.

Securing semiconductor supply chain resilience and longevity will be essential for any automotive manufacturer and their tiered suppliers.

How do you plan for unexpected component obsolescence?

De-risking future production and after-market supply chains through information sharing

De-risking the automotive production supply chain to mitigate the impact of any future supply crisis requires a complete understanding of the semiconductor usage throughout the platform, investment in additional safety stocks in the normal supply channel, and the ability to quickly switch on other authorized sources of supply in times of crisis. Rochester Electronics’ stock of over five billion authorized, active devices provide an instant supply lifeline without the risk of poor quality, counterfeit, or malware from non-authorized sources.

Long-term after-market commitments are characterized by very uncertain, small, and intermittent requirements. OCMs are increasingly partnering with authorized after-market manufacturers such as Rochester Electronics to provide their automotive customers with accurate end-to-end lifecycle coverage. An authorized after-market partner can offer a safety-net supply of discontinued finished goods, transitioning to a long-term build from wafer. Rochester also provides fully autonomous long-term support for the associated test platforms and older semiconductor packages, ensuring 100% compliance with the original specification within a TS16949-approved environment.

Therefore, OCMs can offer a 100% guarantee of component availability, covering production and after-market commitments, without tying up their capital and resources.

With careful planning and early engagement with the OCM and Rochester Electronics, automotive customers have the prospect of avoiding the worst costs associated with:

- Expensive long-term storage.

- Uncertain yield after many years of storage.

- A rigid or fixed forecast LTB qty tied to an increasingly uncertain future.

- A high-risk temptation exists to bridge gaps in the supply chain with non-authorized products.

By sharing usage information with Rochester Electronics, automotive customers gain vital early warning of supply risks, first access to authorized security stocks in times of crisis, and the ability to influence Rochester’s obsolescence investments in stocks, wafers, and ongoing production capacity.

As with all automotive products, quality, reliability, and longevity are vital when sourcing components, requiring trusted partnerships. Rochester focuses on providing a continuous source of semiconductors that aligns strongly with automotive manufacturers' long lifecycle and quality requirements.

Rochester provides a 100% authorized stock of active and EOL devices from over 70 leading semiconductor manufacturers. As a licensed semiconductor manufacturer, Rochester has manufactured over 20,000 device types. With over 12 billion die in stock, Rochester has the capability to manufacture over 70,000 device types.

Rochester Electronics is registered to manufacture ITAR (International Traffic in Arms Regulations) products. Rochester is certified in ISO 9001, Automotive IATF 16949, AS9120, and ISO 14001 (environmental management). It is also QML MIL-PRF-38535 certified for Class Q and V for high-reliability defense and aerospace applications.

The Rochester Electronics’ Semiconductor Lifecycle Solution™ keeps businesses moving.

Learn more about Rochester’s automotive device portfolio

Explore Rochester Electronics’ comprehensive product lifecycle solutions

Rochester’s semiconductor support for the automotive industry

Manufacturers